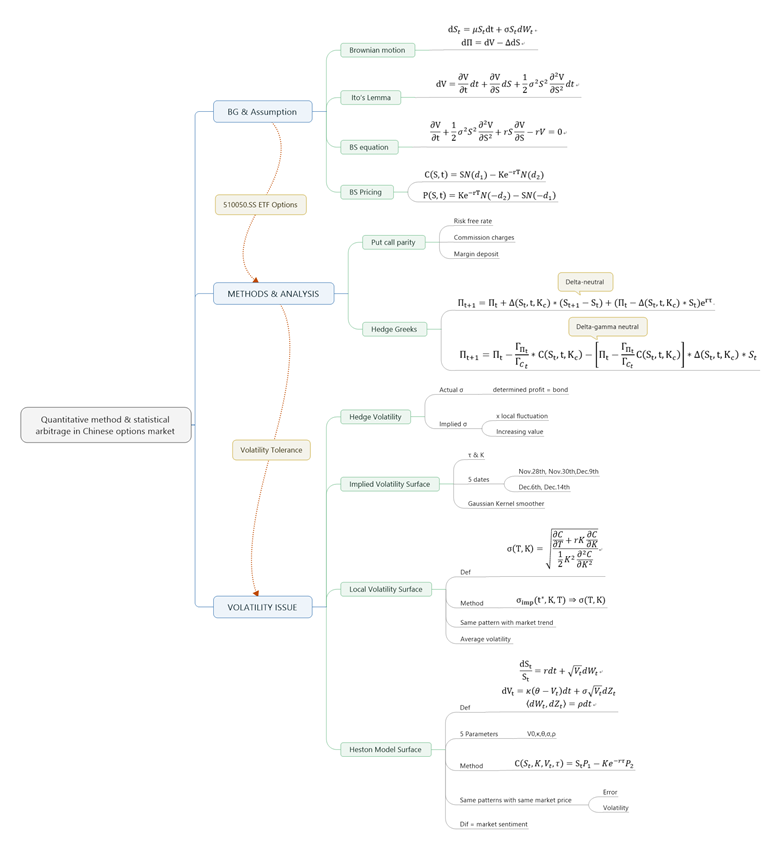

"Quantitative Method and Statistical Arbitrage in Chinese Options Market aiming at 510050.SS ETF options", Honors Thesis in International Business

Purpose – Using quantitative method to analyze options series underlying at 510050.SS ETF, deploying two hedging strategy belongs to statistical arbitrage to test its profitability on certain financial instruments, and further investigating volatility patterns.

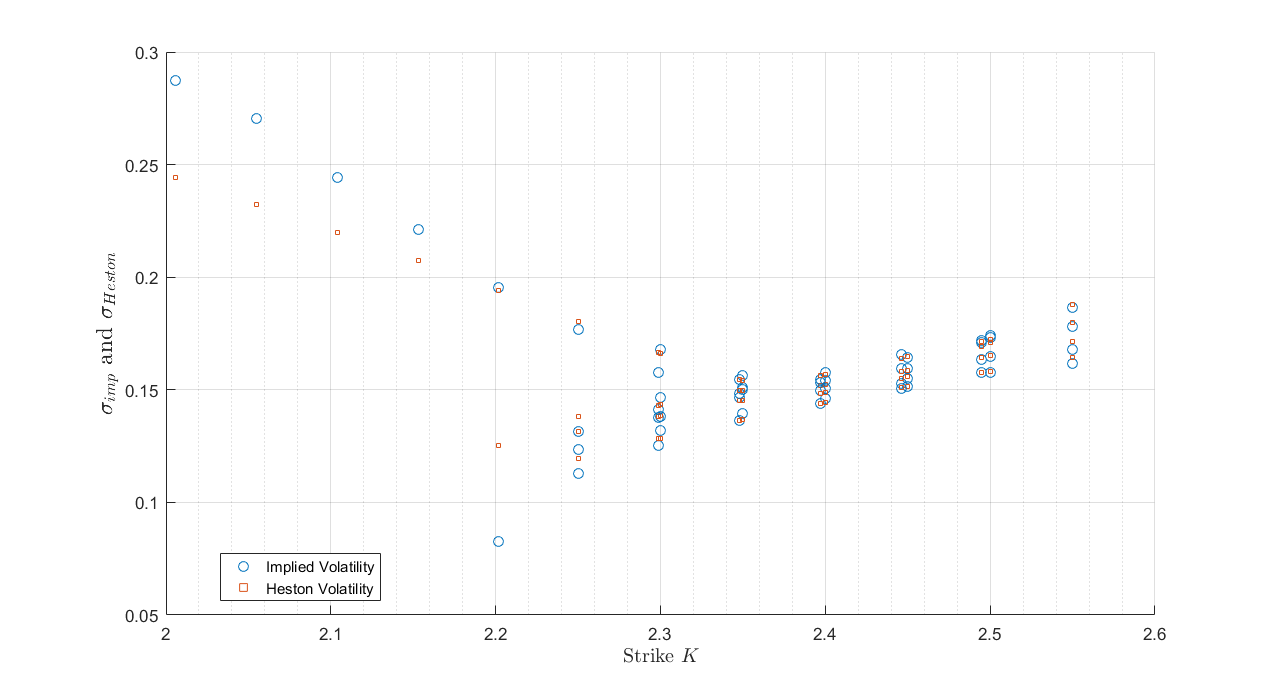

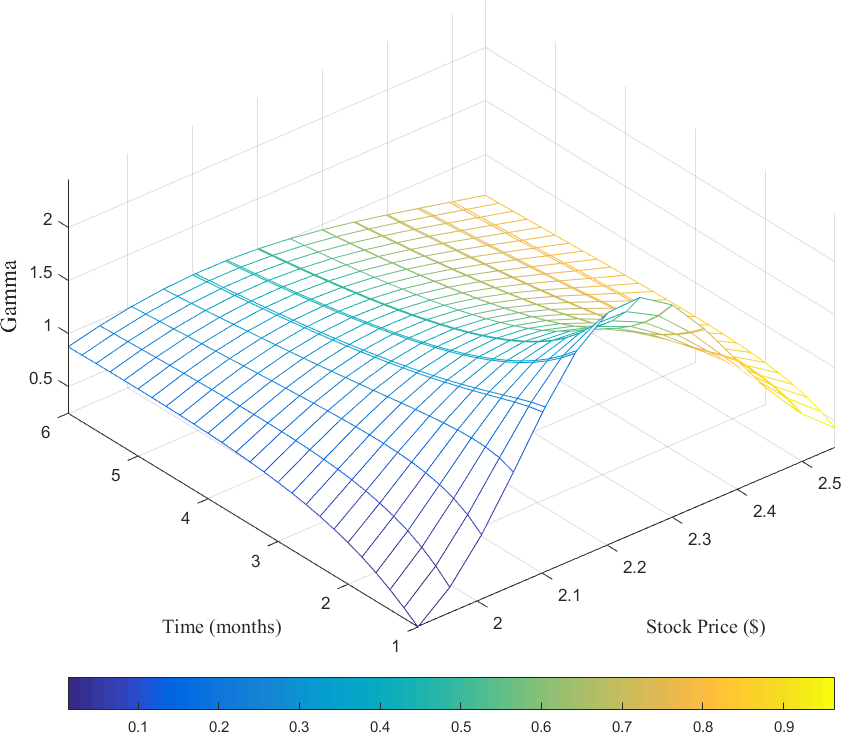

Design/methodology/approach – Analyzing the specific risk and P&L indicator of the options, and conducting a simulation of Greeks neutral hedging strategy then indicating the importance of volatility in arbitrage. Options market data set are used to constructing the volatility surface with local and stochastic volatility, which gives us an overlook to the option market implied volatility along with the analysis of the different surface structures.

Research limitations – The daily data we examined are in low frequency which might be unable to keep pace with options trading mechanism. Also, the term structure of volatility surface may overfitted with limited market products available. Further, only two common hedging strategy with Greeks are handled in this paper, which needs further research on Vega featuring stochastic volatility model and the volatility behavior in market practice.

Originality/value –The theoretical framework shows a feasible way to identify the profitability of Greeks neutral strategies and the specific lime light on which should be laid among aspects of option traders. Two classical volatility surfaces well supports observation market implied volatility, filling the gap lacking available market instruments. And this structure of idea can also be widely-used in the related problems of certain exotics pricing and statistical trading.

Keywords: delta-gamma hedging; Heston model; local volatility surface; Chinese options market

Paper Outline